My three interesting things this month…

1. Moving AI past pilots and productivity hacks

A year ago, most finance teams would have considered it a win if even half of their people were using AI occasionally. Today, that level of adoption feels a lot less like progress.

The tools have changed an incredible amount. AI is faster, more reliable and starting to appear inside the systems finance already use.

But a lot of finance teams I speak to are still struggling to see the impact. Often, it comes down to one of two reasons:

Using AI as an individual productivity hack

The first wave of AI adoption was understandably focused on quick wins (summarise this, draft that, speed up my research), so it’s not surprising that a lot of teams get stuck here.

Using AI to speed up certain tasks isn’t a bad thing. If AI gives someone back 20 minutes a day, that matters.

The issue is when teams stop there. Finance transformation doesn’t come from making isolated tasks slightly quicker, but from looking at the bigger picture and asking what processes should run differently.

Testing AI but never moving beyond the pilot

The other obstacle I see is teams who are genuinely excited about AI, but can’t seem to move past the pilot stage.

Pilots show a curiosity and willingness to experiment that we want to encourage. The problem appears when “we’re piloting a lot of things” becomes a comfort blanket. Teams stay busy with demos without deciding what should become standard.

Why this matters and what finance leaders can do

When AI stays at the level of personal productivity or endless pilots, the impact remains small and uneven.

People start asking whether AI is really worth the effort, when the real issue is often not the technology but the way adoption is being approached.

This is the point to step back and get more intentional about where AI can genuinely improve how the team works. Here are a few practical places to start.

1) Reframe the thinking

A big part of this comes down to what people think AI is for. If the team sees it only as a personal productivity tool, progress will stall.

The conversation needs to move from “How can I save 20 minutes?” to “What recurring work should now run differently?”

It can help to show the team real examples that are directly relevant to finance. Practical examples make it easier to see what’s possible, and OpenAI’s ChatGPT for Finance is a useful starting point for this.

2) Build momentum

People are much more likely to buy into AI when they can feel the results. The quickest way to get there is to choose one frustrating, repeatable process and redesign how it works.

This is different from helping one person do their part faster. One person using AI to draft monthly commentary is helpful. Get your teams to sit down together for 30 minutes per month and put one annoying process into AI – asking how could we improve it with low-code or no-code technology we already pay for.

3) Turn experiments into habits

The finance teams that get the most value from AI will be the ones that turn a small number of useful experiments into better ways of working.

If you’re trying to work out where AI can genuinely make a difference in your finance team, start with one process, improve how it runs and turn it into a new habit. And if you’d like help figuring out what that could look like for your team, get in touch.

2. The hidden leadership cost of being too helpful

I work with a lot of finance professionals who are ready to take their next step. They have the experience, talent and commercial awareness to progress, but find themselves stuck for a reason that is easy to miss:

They’re too useful in their current role. They know the details, spot the gaps, fix the draft and answer the stakeholder question.

Stepping in feels helpful, especially when the deadline is close, but it eventually creates a problem. When too much depends on your input, approval or last-minute rescue, you become the point of dependency.

Progression often requires you to stop being the answer to everything and start removing yourself from work the team is ready to own.

When helpful becomes a bottleneck

Every time you step in to fix a model, rewrite a deck or sharpen an analysis, it can feel like you’re raising the standard.

Finance has tight deadlines, senior stakeholders and a low tolerance for mistakes, so it’s completely understandable why leaders take work back. The problem is what happens next.

- The person who brought you the work doesn’t learn how to close the gap.

- The team gets used to difficult work moving back up the chain.

- You lose time that should be spent on broader priorities.

The extra hours are only part of the cost. The bigger issue is that the team learns to bring the hard bits back to you.

Build a team that can absorb your work

A big leadership goal is building a team that can take more of the work from you. This means being clearer about what really needs your input and what the team could start owning without you.

The leaders who progress fastest are the ones making themselves less needed in the day-to-day. They help their teams build enough confidence and judgement to bring stronger work back, without waiting to be rescued.

So how do you make yourself less needed in practice?

The skill of good delegation is learning how to stay involved without taking over.

A lot of that comes down to the questions you ask. “Have you thought about doing X?” sounds like a question, but it’s actually offering advice in question form.

A better starting point is to use more “what” and “how” questions. They’re harder to answer with a simple yes or no, and they encourage the other person to form a view before you add yours.

For example, instead of asking, “Have you thought about leading with the forecast risk?”, try, “What do you think the main message should be?”

Or instead of, “Could you add more detail for the stakeholder?”, ask, “What would make this more useful for them?”

Finance leaders often have useful context, and there’ll be moments where clear direction is needed. Make them do more of the thinking first, then add your view.

Over time, this builds stronger judgement and more ownership across the team. People learn how to improve the work themselves, rather than waiting for you to fix it.

3. Great finance leadership is often trade-off leadership

Some of the hardest moments in finance leadership come down to one simple question: What matters most right now?

It might be workload pressure, stakeholder demands, competing deadlines, a team feeling stretched or another “quick” request that somehow becomes half a day’s work.

Sound familiar?

Finance sits close to so many important decisions: investment, cost, headcount, pricing, transformation, reporting priorities and performance conversations.

That gives us a real opportunity.

Good business partnering helps the business understand its options, make better choices and stay honest about what limited time, money and energy can actually support.

The challenge is that trade-offs require someone to make a call. And no one really wants to say:

- “This report matters less this month.”

- “That project needs to slow down.”

- “This request is not the best use of finance time.”

So everything stays important, everyone gets a yes and the team absorbs the pressure.

But hidden trade-offs always show up somewhere. Usually as rushed work, unclear priorities, late nights, avoidable mistakes or decisions that drift.

Make the trade-off visible

One of the most useful things a finance leader can do is bring these choices into the open. A couple of questions I like:

“If this new analysis matters, what are we comfortable making lighter this month?”

Or:

“What decision will this work actually help us make?”

That second one is especially useful. As finance people, we can be very good at producing things because they have always been produced. A pack, a report, a dashboard, a tracker. Before long, there is a whole ecosystem of recurring work that nobody has properly challenged for years.

So it is worth asking:

Is this helping someone make a better decision? If yes, brilliant. Let’s make it valuable.

If no, can we simplify it, automate it, reduce the frequency or stop doing it altogether?

I know that can feel uncomfortable. But so is asking your team to keep carrying work that no longer creates enough value.

A simple way to prioritise

As a person who loves finance, I love a good framework!

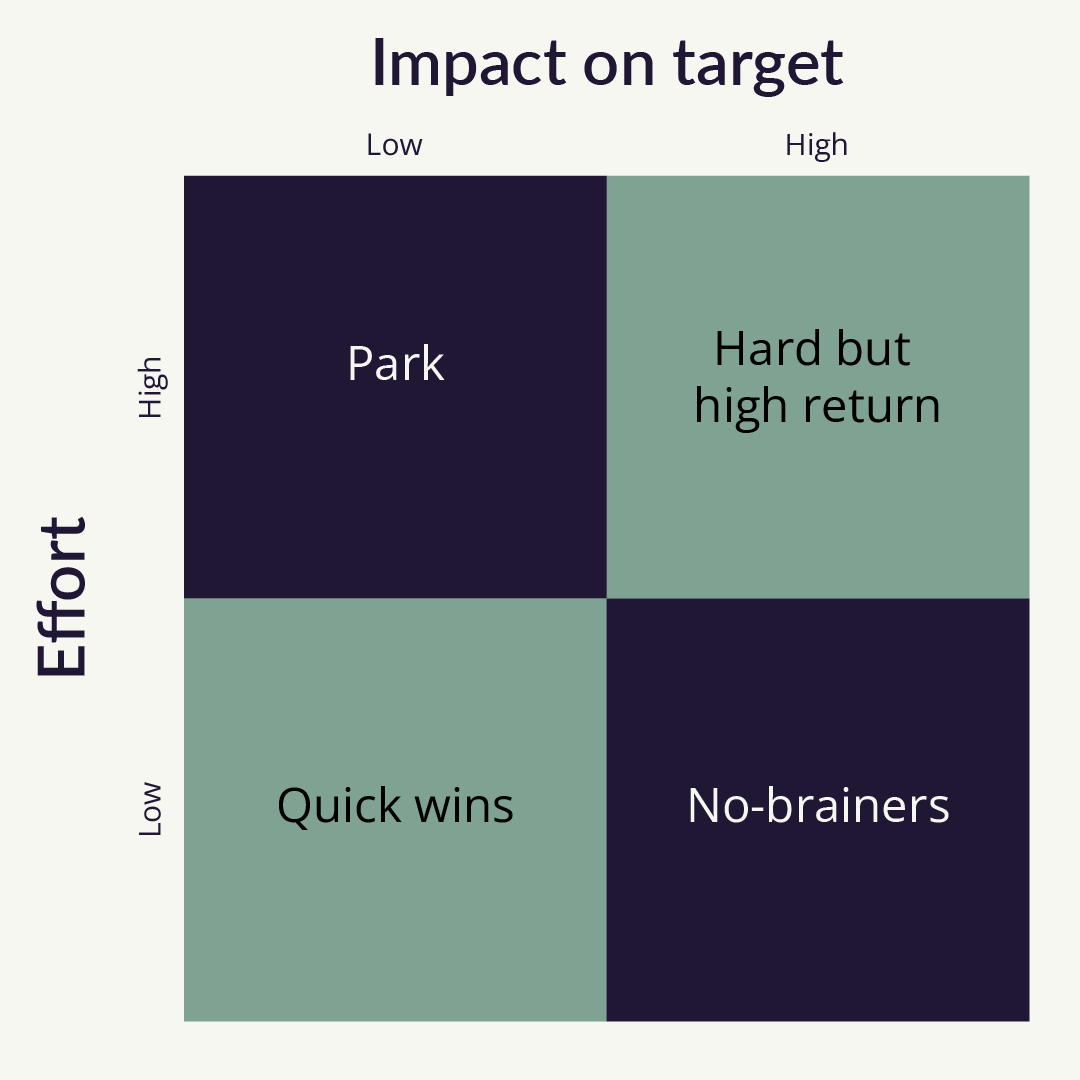

When everything feels urgent, try using an effort and impact view with your team. It helps everyone step back and ask two questions:

- How much effort will this take?

- How much impact will it have?

That usually gives you four types of work.

- Low effort, high impact: do it. These are the no-brainers.

- Low effort, low impact: useful sometimes, but be careful. Too many quick wins can quietly eat the week.

- High effort, high impact: worth a proper discussion. These are the bigger projects that need clear ownership and a good reason for the effort.

- High effort, low impact: this is where leaders need to be honest. Park it, simplify it, automate it or challenge it.

Often, the biggest opportunity is hiding in that last group.

The work may have started for a good reason, but the business might have moved on. Or it may have slowly turned into a monthly ritual that nobody quite knows how to stop. We’ve all seen those!

Create focus

Saying no for the sake of it is rarely helpful. The aim is to create focus.

Finance teams are brilliant at absorbing pressure. Sometimes too brilliant. But when every request is treated as equally important, the real priorities become harder to see.

So next time your team is stretched, try not to start with: “How do we fit all of this in?”

Start with: “What matters most right now?”

And just as importantly: “What are we choosing to make lighter?”

Often, what people need from finance leadership is just a clearer view of what matters most – what we are choosing to do and what we’re not.

Want more insights like this?

Sign up to my interesting things newsletter for monthly updates.